By Miklos Nagy

By Miklos Nagy

Fee-Only Financial Planner & Blogger Business Edge Media

The Smith Manoeuvre is a financial strategy which was first coined by Fraser Smith, a BC-based financial planner. He wrote a book on the subject with the title: “The Smith Manoeuvre” in the early 2000s.

The Smith Manoeuvre is a relatively simple idea, that is to convert a mortgage to an investment loan over time and in so doing transform your non-tax deductible mortgage interest payments to tax-deductible investment loan interest payments.

To implement this strategy, you need a re-advanceable mortgage, consisting of your regular traditional mortgage and a Home Equity Line of Credit (“HELOC”). At any one point of time the sum of the remaining balance of your mortgage and the limit of your HELOC is constant, typically 60% or 65% of your home’s value at the start.

In other words, this type of arrangement allows your HELOC’s limit to be a certain percentage of your home’s value, in the beginning, less the current mortgage balance on your property. As you make your mortgage payments, your principal is paid down on your mortgage. Your HELOC’s limit will be increased by the same amount of principal you are paying off at each mortgage payment. The strategy is to invest these increases in your HELOC in dividend and/or interest-earning investments and so doing making the interest payments on your HELOC tax-deductible.

By doing this repeatedly until your mortgage is paid off, you will eventually fully convert your non-tax-deductible mortgage interest payments to tax-deductible interest payments on your HELOC. For this strategy to work, you need to invest in investments which have a reasonable expectation of earning interest or dividend income. If you invest to make capital gains and no interest or dividends, your interest payments will not be tax-deductible. The investments can be managed portfolios invested in stocks that will pay you a dividend, dividend mutual funds, income-producing rental properties or private first, second (or third) mortgages.

With the Smith Manoeuvre, you will be able to pay off your mortgage much sooner and could build a substantial net equity, in addition to the value of your initially mortgaged property, at the point of time of your mortgage original end of its amortization period (most of the mortgages are for either 25 or 30 years long at the start).

For the strategy to work to your favour, you need to realize a minimum of 2% annual average growth rate on your investment, provided that your dividend yield will be around the historical average of around 3% per annum and the average interest rate on your HELOC not to exceed 5.5%. According to Statistics Canada, the S&P/TSX had an average annualized rate of return of close to 6.00%, excluding dividend yield, between January, 1960 and May, 2019.

Equity mutual funds’ annual management fees are at around 2.50%. If you invest your investment loan in Canadian dividend earning equity mutual funds and will average no better than the market before management fees, in the long term, you will likely average 3.50% or less after management fees and excluding dividends. It is also important to note that most mutual fund managers have historically been underperforming their respective benchmarks.

On the other hand, if history is indicative of the future and having your portfolio managed by a portfolio manager, your annual fees can be around 1.50% and hence your net annualized growth could be about 4.50% plus an average of 3.00% dividend yield.

Interest on your HELOC is tied to the Prime Rate (currently 3.95%) and depending on your creditworthiness can range between P+0.00% to P+2.00%. At present, you could obtain a 5 year fixed closed mortgage at the rate of 2.75% and HELOC with 3.95% interest rates.

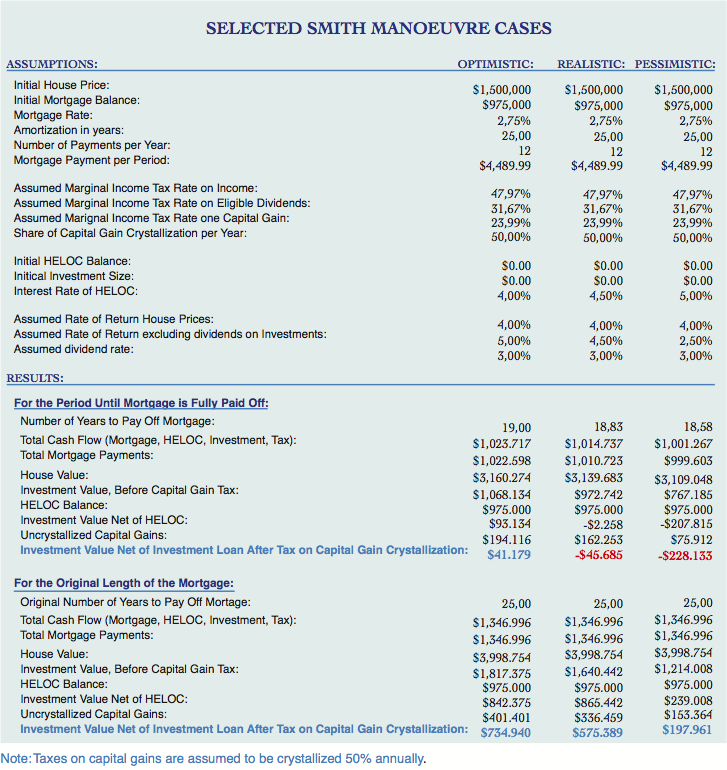

There are several variations on the Smith Manoeuvre. The main, and in my opinion, the best, strategy to follow is to use the tax refunds and dividend payments to reduce your mortgage principal. Then reborrow, using your HELOC, the total of these principal reductions. These principal reductions will reduce your mortgage balance in excess to your regular monthly mortgage principal reductions attributed to your regular mortgage payments. If the tax refunds turn into tax payables, due to crystallization on capital gains and dividend taxes, use your dividend payments to the extent that your cash ow will not increase beyond the original monthly mortgage payments calculated on the length of the amortization period (either 25 or 30 years). Following this strategy, the effect of the Smith Manoeuvre on your net worth can be very substantial as the table above on the following page demonstrates.

As per the table on the following top page, employing the Smith Manoeuvre could make you over $700,000 richer over a 25 years period, assuming that you convert, over time, your initial mortgage of 65% ($975,000) of the current house value ($1.5 million) to a tax-deductible interest HELOC. The exact amount of how much you will benefit from this strategy is dependent on several factors. Keep in mind, your benefit could be significantly less should interest rates substantially rise or stocks perform considerably poorer than that in the past. Also, your benefit could be more. For a full set of the assumptions related to the above table, please contact Fin-Plan.

The table to the right shows figures based on investing in dividend earning Canadian equities. You could also invest in dividend earning US equities or in 1st, 2nd and 3rd private mortgages instead of equities or a combination of all these mentioned. In the long term, US equities outperformed Canadian equities by a large enough margin to consider them as potential investments implementing your Smith Manoeuvre. This is despite the less favourable tax treatment on US dividends and the foreign exchange risk these investments would entail.

The table to the right shows figures based on investing in dividend earning Canadian equities. You could also invest in dividend earning US equities or in 1st, 2nd and 3rd private mortgages instead of equities or a combination of all these mentioned. In the long term, US equities outperformed Canadian equities by a large enough margin to consider them as potential investments implementing your Smith Manoeuvre. This is despite the less favourable tax treatment on US dividends and the foreign exchange risk these investments would entail.

Currently, investing in 1st, 2nd and 3rd mortgages could give you a yield of between 6.00% and 14.00%. These yields are high enough that, despite interest income being taxed at the highest rate and without any ability to defer taxes on any portion of them, they should also be considered as options. I will analyze the Smith Manoeuvre's performance assuming investment in US dividend earning equities and/or Canadian mortgages instead of Canadian dividend earning equities in one or more of my future blogs.

Your gain (or loss) from the Smith Manoeuvre is dependent on your mortgage rate, HELOC interest rate, rate of return on your investments, excluding dividends, and dividend yield. Given that the long term performance of the S&P TSX was around 6.00%, excluding dividends, the dividend yields have been on average approximately 3.00% and assuming you deal with a portfolio manager charging 1.50% annual management fee, the assumed growth rate, excluding dividends, of 4.50% seems to be a realistic growth target. Interest rates on HELOCs will likely be low for the foreseeable future as any significant rise in interest rates will likely impact the Canadian economy too harshly. In my opinion, for the next 20 – 25 years your HELOC rates will average between 4.00% and 6.00%.

The drawback of this strategy is that your overall debt level will stay the same and therefore, you will generally carry a higher level of risk. This increased risk is mitigated by the fact that instead of relying on real estate prices to increase, your portfolio will be diversified into a mix of real estate and equity investments. Keep in mind that regardless of the Canadian real estate price boom in the past 25 years, especially in the GTA and Vancouver, there is a risk of significantly lower growth rates in real estate for the next decades. Toronto and Vancouver have been consistently in the 10 most expensive cities in the world.

Determining whether the Smith Manoeuvre is the right strategy for you needs careful analysis and planning. Fin-Plan can help you in this regard. To ask any question about this article or to book an appointment to look at your particular case, please contact Miklos at nagy@fin-plan.ca. Miklos is a fee-only financial planner, best selling author, finance-related educational course writer, statistician and former Chair of the Canadian Institute of Financial Planners with over 25 years of experience in financial planning for high net-worth and middle-class Canadians. His Fee-Only financial planning website is at www.fin-plan.ca and his LinkedIn page is at https://www.linkedin.com/in/miklos-nagy-fee-only-financial-planner/.