Miklos A. Nagy

Miklos A. Nagy

Business Edge Media

At the time of writing this piece, there are more than 3 million confirmed cases of COVID-19 worldwide with 209,000+ deaths attributed to the disease. By the time the virus is contained or has run its course, the number of infected worldwide could be in the hundreds of millions with millions of deaths. The effect of this coronavirus will be felt for many years to come.

While the virus is causing tragedies in many families and anguish for the population worldwide, it has profound economic consequences as well. As governments around the globe shut down their economies to contain the virus, a large percentage of formerly employed people are now finding themselves without a job, either temporarily or long term. Governments adopted extraordinary measures in the hopes of averting deep, long-term recessions or depression by offering substantial financial assistance to a large percentage of their populations. The amount of COVID-19-related aid is in the trillions of dollars for the U.S. alone and more than $200 billion in Canada.

A likely effect of this massive amount of money handed to the unemployed is inflation. Almost all of the countries in the world are printing vast amounts of money to help citizens unable to work. This makes inflation much more probable compared to if it was happening in just a few countries.

Because of the increased likelihood of a high inflationary period ahead, I was interested in how different asset classes performed in inflationary and non-inflationary periods in the past. I looked at their respective historical annual returns and their correlation with the corresponding consumer price index (CPI) in the same year, the next year and two years later, making sure that one-year or two-year lagged effect of inflationary years are also analysed.

The period I selected is starting 1961 through 2019 with one exception; the timeframe is 1968-2019 for gold because the gold price was fixed before 1968. The type of assets that I analysed and my source of historical data are the following:

- S&P 500 (source: Yahoo Finance)

- S&P TSX (source: Statistics Canada till 1979 and Yahoo Finance after that)

- Gold Prices in US$ (source: www.datahub.io)

- Home Prices in the GTA (source: TREB monthly Market Watch)

I used the historical Canadian and U.S. annual CPI figures for inflation as published on the website www.inflation.eu . The years that had inflation above 3% I classified as inflationary years and the rest as non-inflationary years.

I did not analyse correlation and return characteristics of government and corporate bonds as bonds generally are negatively correlated with inflation and perform markedly worse in high inflationary periods. The prices of bonds depreciate as inflation and interest rates rise.

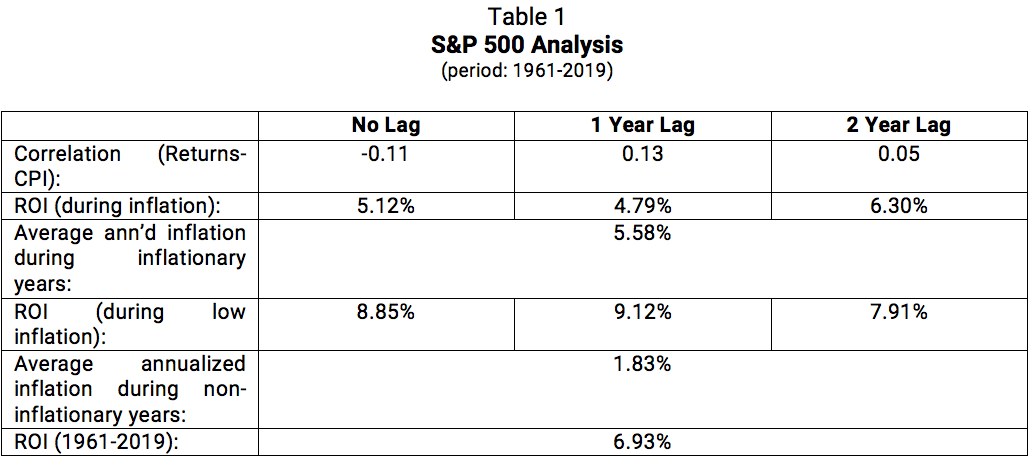

In Table 1, the S&P 500 index annual returns showed either slightly negative or very low correlation with inflation regardless of the lag. Furthermore, its annualized rate of return (note that reinvested dividends are not taken into consideration) was lower in inflationary years than those of non-inflationary years.

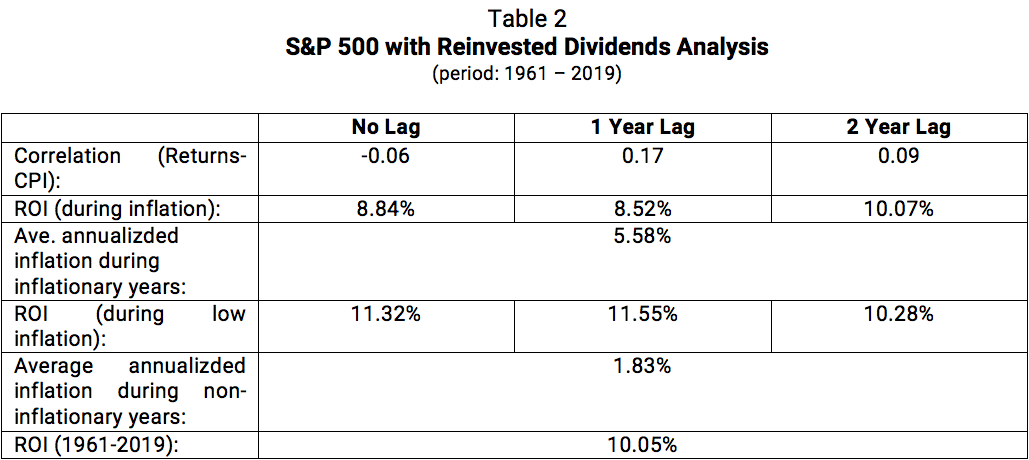

In Table 2, S&P 500 with reinvested dividends also had annual returns that showed either slightly negative or very low correlation with inflation regardless of the lag. Furthermore, its annualized rate of return was significantly lower in inflationary years than those of non-inflationary years, except when assuming two-year lags of the inflation’s effect on the index with dividend returns.

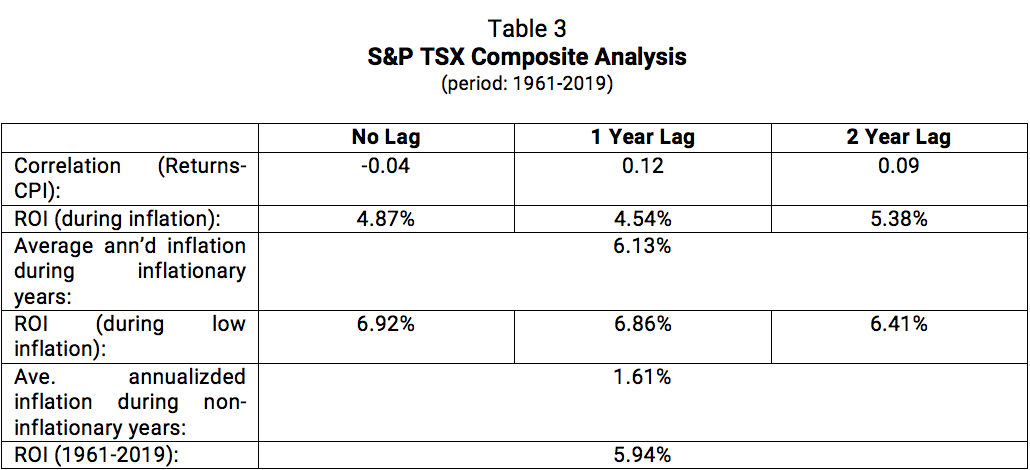

In Table 3, S&P TSX Composite, reinvested dividends are not taken into account, also had annual returns that showed either slightly negative or very low correlation with inflation regardless of the lag. Furthermore, similar to that of the S&P 500, its annualized rate of return was lower in inflationary years than those during non-inflationary years.

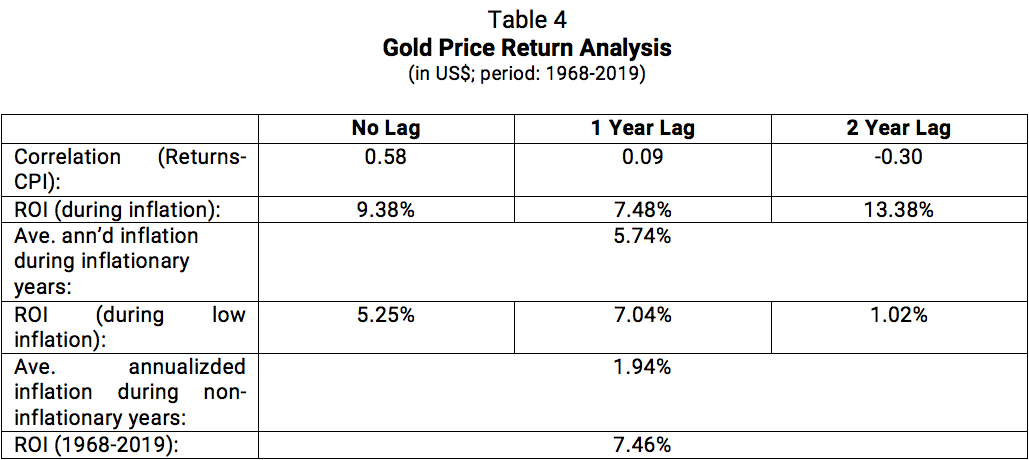

Table 4 shows the analysis of returns on investing in gold. Gold with no lag shows a strong positive correlation with inflation. Gold prices have increased significantly more during inflationary years and during 1 or 2 “lagged” years. Surprisingly, it shows the best annualized performance in inflationary years with 2-year lags (13.38%).

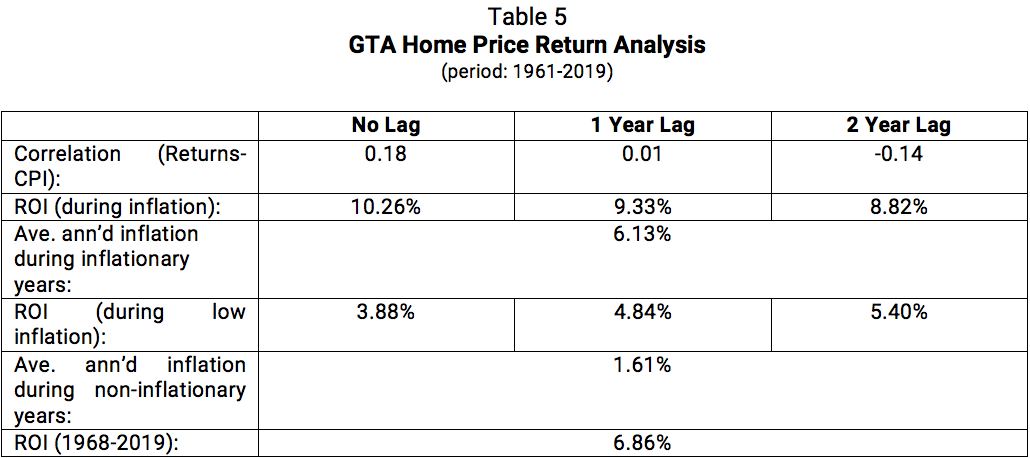

In Table 5, I analysed returns on investing in single-family homes located in the GTA from 1961 to 2019. While returns on GTA housing do not show a high positive correlation with inflation, it had significantly higher annualized returns in inflationary years (with lag or without) than those in non-inlationary years. Among all of the analysed asset types, the average excess return over the average annualized inflation is the highest (4.13%; 10.26% - 6.13%). One needs to treat the GTA return figures with caution as the GTA area has somewhat expanded over time, the type of dwellings composition has been changing (eg. condo sales now account for a lot larger percentage of the sales today than those 20-30 years ago) and the distribution of the actual sales within the different neighbourhoods of the GTA is obviously will not be the same from one month or year to the next. Also, prior to 1965, average home prices were calculated on all types of sold properties not only on single-family type of sold housing units. Having said this, the vast majority of sales have been single-family homes. Nevertheless, I believe that the GTA average home price returns were likely very close to the returns calculated from the available data.

The risk of inflation is high in the coming years. Assuming that this will happen, in my opinion, the best actions what you can make to increase your expected rate of return are the following:

- Increase (or introduce) your investment in gold to 10-20%; and

- Increase your investment in real estate, finance it with the currently low long-term mortgage rate (provided you live in the GTA or VTA); and

- Eliminate your mid- and long-term bond investment; and

- Maintain or reduce your stock market investment by up to 20%.

Determining what percentage of your portfolio should be invested in different asset classes needs careful analysis and planning. Fin-Plan can help you in this regard. To ask any question about this article or to book an appointment to look at your particular case, contact Miklos at nagy@fin-plan.ca. Miklos is a fee-only financial planner, best-selling author, finance-related educational course writer, statistician and former Chair of the Canadian Institute of Financial Planners with more than 25 years of experience in financial planning for high-net-worth and middle-class Canadians. His Fee-Only financial planning website is at www.fin-plan.ca and his LinkedIn page is https://www.linkedin.com/in/miklos-nagy-fee-only-financial-planner/.

The views expressed in this article are the opinions of Miklos A. Nagy through the period ended 04/22/2020 and are subject to change based on market and/or other conditions. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statement is not a guarantee of future performance and actual results or developments may differ materially from those projected.

Investing involves risk, including the risk of loss of principal. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed.

All rights reserved. No part of this article may be reproduced, distributed, or transmitted in any form or by any means, including photocopying, recording, or other electronic or mechanical methods, without prior written permission of the author, except in the case of brief quotations embodied in critical reviews and certain other noncommercial uses permitted by copyright law. For permission requests, write to nagy@fin-plan.ca.